First off, I have to tell you two stories.

One: on December 13, 2008, pretty much one of the worst weeks in market history, my publisher decided that should be the launch date of a book I wrote.

The book was called “The Forever Portfolio” and it was about the stocks I felt that people should buy and hold forever.

Nobody bought the book. That’s not true. At last count, 299 people bought the book.

Nobody wanted to hear about buying stocks forever. People were selling stocks and not looking back.

I was scared also. I had started a new hedge fund in September 2009. But the hedge fund that funded me got too scared and decided at the end of October to stop the experiment.

I really thought all aspects of my career were over. Plus, I had recently sold a company for all stock and that stock had gone from 13 to 7 and I had just bought a home (against all of my later advice) .

So what happened. The guys at Choose Yourself Media did an analysis the stocks in the Forever Portfolio have gone up X% and the stocks in the Dow Jones Market Average have gone up Y%. In the past 5 years I have (luckily I have to admit) outperformed the market (and Warren Buffett) by Z%.

I don’t say this to brag. I got lucky. I was so scared I couldn’t sleep. I would go on the Erin Burnett Show on CNBC every Tuesday and during the half hour I was on the show the Dow would go down another 500 points. Every week. I thought I was going to throw up all the time.

Second story: Fidelity used to ask me to give talks to their clients four times a year. Sometimes more.

That February (2010), I was getting a divorce, I was still scared, and I had just gotten fired from the company that bought my prior company. So no income and no prospects in site.

500 people were in the audience. I’m sure some of the readers of this newsletter were in the audience .

I outlined all the reasons the market was going to go up. First, in the back office, I told all the Fidelity professional why I thought the market was going to go up. One woman literally started crying and saying, “thank you. Even if you are dead wrong I need some hope.” Fortunately I was not wrong.

OH! I have a third story.

I forget the exact day. It was a year or two later. Maybe 2011. July 5 or 6th. I was debating Nouriel Roubini. He said the market was going to go 20-50% down from that point.

I said it was going to go straight up.

Again, I got lucky. It went straight up.

This sounds like I’m bragging (I guess I am a little) but I do a lot of research. An enormous amount of research. It’s my family’s livelihood at stake because I make my living by investing. I don’t make it off fees or scams or going on TV or books. I invest.

But I’m a bit lucky. Because a lot of people do research. What I’m going to do is in A through Z, summarize some of the research.

Since these are bullets and we are only limited to about a billion or so words it might not be totally comprehensive but maybe we can figure out a way (perhaps on a podcast) I can answer any questions you might have afterwards.

By the way, a top Director at the Swiss bank, Credit Suisse, wrote to Nouriel Roubini about a year later and said, “Looks like James was right. When are you going to invite him to one of your famous parties.”

Roubini was well-known for having blow-out parties. I didn’t want to go anyway (I’m more of a cave-man) but I was curious what his response would be.

He did write back, to his credit, and said, “Next time there is a recession.”

Well, we’re all still waiting.

A Through Z of what you need to know about the recent market crash.

A) Since 1955, if the market is down for six months, it’s on average positive one year later.

I don’t like statistics like this because there are too few examples Suffice to say, we’ve been here before, we’ll be here again, and usually the market is higher a year later.

B) The market is down, in part, because of fears that China’s economy is falling.

China has grown 10% per year for 30 years. Now it’s growing about 5%.

A couple of points. That’s GROWTH of 5%, even though it’s slowing.

Also, much of their growth was funded by our bonds, which they have been consistently paying back BECAUSE of their growth. And a lot of their growth has come from building first-world products that our innovation has developed.

They are the second largest economy in the world. But let’s not forget: in 1989, Japan was the second largest company in the world. That was the highest Japan ever was. Meanwhile, we keep growing. The US has been the source of innovation for both Japan and China.

But what if China fails?

Ok, so what? Here’s what EVERYONE has failed to mention in the newspaper: China is less than 1% of US exports. China could go to zero (and, one again, they are growing), and we’d still have a growing economy in the US.

C) THE FED

I put it in caps so you say it out loud ominously. People are afraid the Federal Reserve will raise interest rates.

How come? The Federal Reserve interest rates are (very roughly) the interest rate they charge banks. The lower they are, the less banks pay on savings accounts.

So if the Fed raises rates, savings accounts rates go up and people would rather invest in a safe savings account than the high-risk stock market.

OH MAN!

The Fed Funds Rate is 0.25%. I have to put in exclamation point there. 0.25%!

Do you think if they raise it to 0.5% or even 1%, suddenly everyone is going to say, “Man, I better move all my money into a savings account now.

Of course not! In fact, the Fed only raises rates when the economy is going strong, employment is strong and inflation is starting to peak up (which is not happening).

So typically, for at least the first year after the Fed raises rates, often the Stock Market goes UP, not down. And in a case like this, where rates are so low, it will take a long time before the Fed has rates at 6 or 7% where it starts to compete with the average market returns.

I actually hope the Fed raises rates although I think that is not likely given that I am more worried about DEFLATION than inflation right now.

D) P/E ratios

Readers of this newsletter are at all different levels of financial literacy and that’s fine. When I was building my first business I could care less what a P/E ratio was.

Basically, if a company is worth $100 but it’s owners only take $1 a year home in income, then the P/E ration is said to be 100. That’s very high and where all the Internet stocks were in 2000 when they collapsed.

That’s also 1% of what the company is worth. That’s where I’d rather look at savings accounts or bonds.

So a P/E ratio of 100 is bad (1% return) and a P/E ratio of 5 (20% return with Federal Interest rates at 0.25%) is too low. Usually the market is around 15-20, particularly with Federal Interest rates so low.

The stock market’s P/E ratio on average is 19 right now which is high, but not excessive.

BUT, market indices are weighted in favor of the larger companies so we should really be focused on those.

The P/E ratio of:

Apple is 12

Exxon …12

Wal-mart…13

Berkshire Hathaway (Warren Buffett)…18

These are the companies that should tell you if the market is high or low.

How come? Because if the market is lower is Apple going to really trade low enough to give out a 20% dividend? That would be almost impossible. And there is no sign that the growth in these companies is slowing.

Which brings me to:

E) When the entire market goes down 10-15% does that really mean 8000 companies should simultaneously lose 15% of their value? This is why I am always suspicious of media-driven market selloffs.

For instance, Disney, which is about to release the first Star Wars movies in a decade or so, just lost $32 BILLION in value in the past five days.

Really? Is it going to lose another $32 Billion and then release Star Wars which will be the biggest movie in box office history?

F) I know a lot of people are panicking but we have to have a little perspective.

The market has “crashed” and “reeled” according to the headlines at the Wall Street Journal, which I used to write for.

Guess what. It’s down 3% in the past year. 3% is not a crash. That’s what’s called a normal market where stocks go up and down.

And it’s UP about 18% in the past two years. That’s about average. Maybe slightly above average.

This is neither good news or bad news (which is the point). It’s not even news. The market might go lower. But it has not been anything close to a crash and is only called that to scare yu.

G) Warren Buffett likes market like this (I wrote the book “Trade Like Warren Buffett”). Why?

As he puts it: when you go to the grocery store you aren’t hoping that hamburger prices are high. You are hoping they are low.

Unless, of course capitalism is falling apart (which it didn’t even do when it looked like it was in 2008).

When stocks are low, chances are they go up from here. Even in the worst part of the 2008-2009 crash, guess what happened – just a few years later the market was back to all-time highs.

H) Unemployment

When people are employed, they buy more, companies do better, stocks go up.

Looks like people have jobs to go to.

Now, you can argue: look at 2007. They had jobs to go to then and then we had the biggest crash since the Great Depression.

Which is why another number is important.

People can’t buy things if they owe a lot of money.

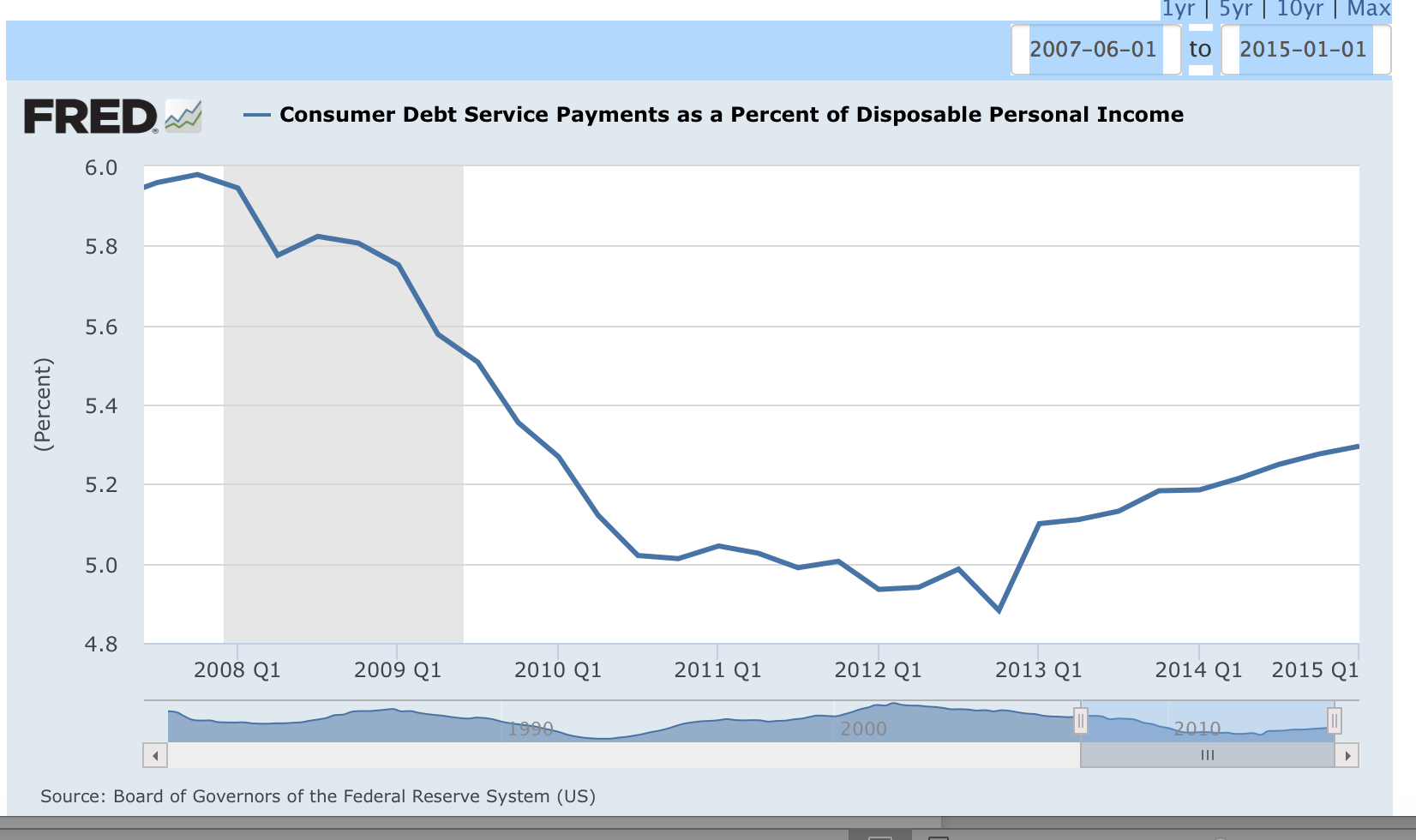

I) Household Debt Obligations.

this is the ratio of how much people’s income goes straight into paying debts.

Here it is, straight from the Fed:

Guess what? More people are employed and we owe less money.

Hey kids, buy those crappy clothes at Forever 21 in the mall!

J) Fear.

Check out this quote by Howard Ruff who regularly appears on CNBC and warns about all the doom and gloom about to happen.

Here’s a quote from Howard Ruff’s book, “How to Prosper from the Coming Bad Years”

Sounds pretty scary! Heck, I’m scared reading it.

It was written in 1979. Right a before a two decade (even a three and a half decade if you count recent all-time highs in the market and economy).

Why did he write this? Because he wanted to scare you.

Here’s what he wrote a few years after that quote:

Fear will only get you so far.

K) OIL

Another thing people are afraid of is that oil is so low.

There’s a cliche: we need to learn history or we will repeat our mistakes.

Unfortunately, even knowing history, we tend to repeat mistakes.

Oil was a massive reason the stock market hit its third worst period in in the past century, in 1973-74 when the OPEC crisis hit.

It’s because Oil was going UP and not down. And OPEC was holding us hostage so we had no idea how high oil was going to go. It was crushing the economy.

Oil at LOW prices is not necessarily a bad thing.

That said, the fears are going to be over. How do I know? Because I invest in oil wells. Meaning I know guys working on the rigs who tell me what happens.

I spoke to a guy who recently went out wildcatting on his own wells who used to be a very high executive at Exxon. He schooled me on Oil.

He said, “James, everyone gets their data rom the EIA. Energy Information Association. We’re all supposed to report how many wells we have drilling. Well, we delay. Between four months and two years. And that’s the data the media gets.”

“The reality is,” he said, “is that oil wells are shutting left and right. They are all shutting down at these prices.”

“So does that mean oil companies are a buy?”

“Maybe,” he said, “but the US also gets oil from elsewhere. Better to buy a company like Apache Resources which has huge investments in natural gas which is also a byproduct of all of these oil wells.”

L) HOGS

I want to tell you a story about fear. In 2009, the World Health Organization issued a pandemic alert on Swine Flu. I don’t want to discount the importance of this. Over 200,000 people died. This is a far cry from the 18 million who died in the 1918 flu pandemic but every life is important.

That’s not why I’m telling this story. I did a video the day of the alert. How come?

Because a stock with the symbol HOGS fell 20% in one day. They were (or are, who cares) China’s biggest pork packager.

Guess what? (I say that a lot but only because the gap between news and reality gets funnier and funnier): you can’t get swine flu by eating pork products.

There was no reason for this company to lose 20% of it value in ONE DAY. It went back up almost immediately.

I am not judging fear as good or bad. And, by the way, I am not recommending people go out and buy the market.

The lesson to be learned from all this is to

a) not panic

b) begin to look for opportunities when people are behaving irrationally.

The market is going to crash much worse than this at some point. If you have an arsenal of good stocks and opportunities that are well-researched then you won’t even waste your time looking at stock prices day to day.

That’s the beauty of good research. That’s why I’ve started thinking about stocks again. Because opportunities like this are starting to happen.

Not short term HOGS-style trades (although those will always be there and I will try to keep people informed of them).

But long-term trades based on the ever-increasing American innovation which can’t be stopped.

Which brings me to:

M) TRENDS

In 2008 the main trend that was happening in the economy was that people were taking out massive mortgages to buy houses and banks were not ready to handle defaults. They had horrible balance sheets. More on that later because it wasn’t as bad as people said.

But now the trends are so much more diverse and the opportunities are so much greater.

Robotics, Drones, 3D Printing, Synthetic Biology, etc are all growing at rates of 100-300% PER YEAR.

That might mean they are small now. But in four or five years you could be 3D printing your driverless car and using a typewriter to type out the DNA for a new prosthetic leg that lets you run sixty miles an hour like the 6 million dollar man.

There are a couple of high-flying stocks (e.g. stocks with the words “3D printing” in them) that I wouldn’t touch. But there are 100s of companies that are the suppliers of the main flagships of these trends.

Again, I’m never in favor of buying the market. Not because I think there’s massive crashes. I just don’t really enjoy watching the ups and downs and having to research all of the idiotic issues in play.

But I love looking at the back doors of these innovative technologies and finding the right plays. They might not work out tomorrow, just like stocks like Amazon and Apple weren’t straight up lines. But they will be huge as the opportunities becomes apparent.

Don’t forget the important rule: if you start with a penny and double it every day, in four days you only have 8 pennies. But in 30 days you have $10.7 million.

This is what happens in explosive industries. The first industry that experienced this growth was technology when Moore’s law in the 60s predicted that chip power would double every year.

Well, he was right. And now everything is run by computers. Your smartphone is a billion times more powerful than the computers on Apollo 11, which went to the moon.

N) Housing

The culprit! The bane of 2008!

Housing fell apart in the last crisis. In fact, housing fell apart in 2006, a full two years before the market fell apart.

So what is happening to housing now, which is a major part of the US economy?

Last month sales of existing homes reached the highest levels since 2009.

Sales of new homes were also up 10% year over year. And with household debt obligations at a low (see above), this industry is not in danger of default. Far from it.

O) The Banking System

Part of the problem in 2008-9 is that the banks technically collapsed. Only a change in the laws plus a massive bailout saved them.

But on several metrics, banks are at their healthiest levels ever:

– chargeoffs (debt that is written off)

– capital in the bank (cash on hand if there is ever a run on the banks (this is a very rough definition)

– number of banks failing the stress tests put in place are at the lowest level since crisis.

So banks aren’t failing.

P) The reason for the crash of 2009

Right now we are feeling post-traumatic stress over 2009. I am, for instance. When the market goes down 10% I call my best friend and ask is the world over. I can’t help it. It’s like a reflex.

But then I start thinking again.

A lot of bad things were happening in 2007-8. Don’t forget that the housing boom ended in 2006, so this wasn’t the real reason for the crash.

What happened that caused the crash.

This is hard to explain but it’s important.

If I owe a bank $100, the bank puts $100 as an asset on its balance sheet. It plans on getting that $100 back from me. If I miss a payment, it still has it at $100.

This may or may not be the correct thing to do. Maybe they should mark it down a little.

But for 100 years they didn’t.

Then in late 2007 (the peak of the market was November, 2007) the Financial Accounting Standards Board changed the rules.

They basically said, “banks have to mark debt where the last price was”.

Imagine if your house is worth $500,000. Your next door neighbor dies and his kids are desperate to sell the house so they sell it for $300,000.

According to the new law in 2007, you would have to “mark” your house at $500,000.

Hedge funds were aware of this and began selling the debt, forcing banks that held similar debt to mark them down because of the new rule, even if there were no defaults (yet).

So banks were no longer meeting the minimal required standards and started to fail. One thing led to another and we didn’t have a housing crisis (which was in 2006), we had a financial crisis (2008-9). Hedge funds made billions. Main Street went bankrupt.

Guess when they changed the rule back: Early March, 2009. The day the market started going straight up again until it hit all time highs.

I’m not saying this is the only reason for what happened. A lot of bad things were happening and, to be fair, banks were over-leveraged (which they aren’t now).

But still, when you change the rules without taking into account what could happen, a crash could happen, which did happen until the situation was reversed.

Nothing like this is remotely happening now. A healthy capitalist system depends on healthy banks. Healthy banks eventually lend to companies doing innovation and that builds new industries and economies go up.

Again, it might not mean the market goes up or down. It just means, don’t panic. Look for your spots. Some sectors will crash, some will go up.

We’re going to experience a lot of ups and downs just like we just did. I don’t say this to scare anyone. Just to get ready for it. I will tell you what I like to do. I don’t always do it but I try.

Q) Don’t do anything

I don’t even look at the newspaper. I watch comedies. Lately I’ve been catching up on the Jim Gaffigan Show. He’s in his first season and it’s very funny. I can’t wait to see him live on December 12 at Madison Square Garden.

When markets go down 10%, some of my smaller stocks go down 30%. I don’t think of it (well, I do a little. I get scared). But the reality is: if the story hasn’t changed, the stock is just going along with market volatility.

R) Use 2-3% of your portfolio.

When I buy a stock, I only use 2-3% of my portfolio. This gives me room to maneuver when the stock goes down and I can buy more. I’ve bought more shares of TROV for instance when it went down once.

I believe in the long term stories of every stock recommended here. And that strategy has served me well and made me a lot of money in the past five years.

But it’s hard not to panic. I basically research my way out of the panic. I admit it.

S) I diversify by hedge fund.

I admit I’m not the smartest guy on the block. The smartest guys have 100 PhDs working for them and people visiting factories in other countries and writing down the license plate numbers in parking lots and so on.

The hedge funds.

So what I do is keep track of their filings and their movements. Watch what stocks they buy wait for the stocks to dip and then it’s as if the hedge fund is working for me, I get a better price, I get total nimble-ness, and I get to pick the best of their picks.

Example: If Warren Buffett buys IBM at $120 and it goes to $100, well I’m fine taking Warren Buffett’s free advice, buying it at a discount to where he buys it, and then riding it out since he’s a long-term holder.

Interesting report: if you JUST piggyback Warren’s picks (and not wait for a discount), even then you would’ve outperformed the stock market by about 10% per year.

T) I don’t daytrade

A situation like HOGS is a very rare example. There are a few other rare examples like that but you have to really be watching for them.

When you daytrade you turn the stock market into a zero-sum game. There are winners and losers.

You’re on one side and I always imagine Vladimir Putin and the top hedge funds on the other side. They are going to win.

Often if a stock goes down people trigger panic. They call me and ask, “are you selling?” and I always ask, “did the story change?” and they say “no, but the stock is down.”

Fine, if the story hasn’t changed and nobody is breaking the law with insider trading (which does happen but you can tell often and avoid it) then I might even buy more.

—

Well, I thought I had up to “Z” but the stock market as a whole is not that interesting. STOCKS are interesting to me.

It’s worth noting that these stocks all started in depressions or recessions:

IBM

General Motors

United Technologies

Hewlett-Packard

Intel

Southwest Airlines

FedEx

Microsoft

Symantec

So even in a recession, you can find opportunities that can create billions in value for early shareholders.

Which begs the question, should people consider angel investing?

Angel investing is when you invest in a private company that may eventually go public.

I’ve had some big successes in angel investing in the past few years but I don’t recommend it.

I think we are entering into one of those rare periods where the cheapest but highest growth companies are going to be found in the public markets, particularly after the recent volatility.

But why would I say that even though I have made good money angel investing? I even advise a top angel investing Venture Capital fund.

I was talking to my friend, Tucker Max, who is a successful angel investor. He’s up maybe 1000% or more from angel investing. In fact, we’ve been in many of the same deals for years.

I asked him what his thoughts were and he graciously wrote them down. We’ve even spoken about some of his investments on my podcast.

Heres what he has to say about angel investing. This can almost be like a bible of angel investing.

—-